Almost 700 registered participants from institutions ranging from A (like ABN Amro) to Z (like Ziraat Bank) filled the conference rooms, formed long queues at the buffet and attended the stands of the numerous exhibitors, including SDS. Read about what made this Meeting the “Best Financial Centre Meeting ever” (Quote: Jens Zinke, Managing Director of WM Group).

SDS REPORT: RegTech for CSR/FATCA. A Snapshot

In addition, corresponding technologies which meet the comprehensive CRS requirements have been implemented. Download the report and read about the new and/or extended requirements to the design, operation and the management of modern technologies for taxes and regulations.

SDS REPORT: Success through agile methods in software testing

At SDS, we have developed an approach to compensate potential weak points which a rigid, linear procedure may entail, and try to unite both worlds, waterfall and the agile procedure.

Get prepared for DAC 6. Wrap-up of the 2018 Operational Taxes for Banks, Europe

The first Infoline conference “Operational Taxes for Banks” took place in London in June. Now a second conference with the same title followed in Zurich, Switzerland in November 2018. In our view, the main topic of this conference was clearly DAC 6, which will be the “next big issue” from a regulatory perspective. It seemed to SDS as if the importance of this topic has not yet been fully recognised by all institutions. We see two reasons why this might be the case.

SDS took part in both conferences as an exhibitor and sponsor. Both conferences have been very informative, with lots of interesting and knowledgeable speakers from all parts of the financial industry and many interesting discussions.

Although both conferences used the same title, it was interesting to see how the topics of the conference have evolved during these few months since the event in London. In our view, the main topic of this conference was clearly DAC 6, which will be the “next big issue” from a regulatory perspective.

However, it seemed to SDS as if the importance of this topic has not yet been fully recognised by all institutions. We see two reasons why this might be the case:

- It is not yet clear which department in a financial institution will be responsible for the implementation, and no department feels responsible. DAC 6 is a reporting requirement, but it is also strongly related to tax, compliance, risk management and even the core business. Depending on the business model of a financial institution and its customer base, the topic could be located in either department, but it is clearly a cross-functional topic which needs to be addressed as such. Clearly, this makes it even more necessary to start thinking about the implications as early as possible.

- Since it is “only” a directive, the EU member states are responsible for the country-specific implementation, and they have to finalise the requirements by the end of 2019 and provide the necessary guidance. This gives financial institutions the feeling that there is still ample time and it is impossible to start now without the final regulations. However, it should be considered that reporting starts in mid-2020. It will be impossible to wait until the end of 2019 and then have a solution ready within half a year.

Financial institutions will have to prepare for DAC 6 much earlier, even if not all requirements are already yet. This is especially true for institutions which are operating in several countries, since it must be expected that the different countries will issue different requirements, a practice to which we are already familiar from CRS reporting.

SDS Software Daten Service strengthens management team with Erste Bank top-manager.

RegTech for CRS/FATCA. A snapshot.

During the last few years, the international financial service sector had to extensively deal with the most important operative tax and regulatory challenges according to CRS. In addition, corresponding technologies which meet the comprehensive CRS requirements have been implemented.

Since the introduction of the Common Reporting Standard (CRS) of the OECD – by signing the multilateral CAA as master agreement in October 2014 – not only a few years have passed by, but also the number of member states grew from originally 51 to 103 (status September 2018).

However, more than half of the CRS countries articulate requests which deviate from the master agreement or partially exceed it significantly. A number of financial institutions are nowadays facing the disillusioning situation that their existing RegTech solutions are not sufficient regarding the range and depth of market-driven requirements.

In the context of this dynamic and increasingly challenging issue there are new and/or extended requirements to the design, operation and the management of modern technologies for taxes and regulations.

High data volumes

Due to the expected accession of further countries to the CRS the necessity of processing high data volumes in bilateral and multilateral exchange relations will increase further. The demand for highly performant solutions which are able to automatically process large data volumes will naturally rise.

High data quality

Especially where different source systems (e.g. by different IT systems from various countries) are used, the requirements to ensure the data quality of source data will grow. This calls for solutions which can detect incorrect data of the source systems and correct data via exception handling in a reliable and automatic way.

High data requirements

More than 50% of the current CRS countries articulated requirements (data requirements or deviating schemes) which deviate from the standard and/or partially go beyond it in a significant way. A modern technology solution must therefore be able to flexibly parameterise different requirements and to create various country-specific schemes.

High reaction rate

Reporting standards can also be changed or extended in productive operations for specific countries during the year. Solution providers who can implement new requirements on time for the next reporting period will become preferred partners.

High complexity

The difference from CRS to FATCA reporting is characterised by a higher complexity and more extensive volumes. Many financial institutions underestimated this essential differentiation for the selection or implementation of their technology solution. They notice that the extension of FATCA solutions partially developed by themselves has no perspective and is not feasible due to missing practicability. Therefore, they recognise the necessity to replace them by modern and comprehensive standard software.

Summary

Since the introduction of the Common Reporting Standard (CRS) of the OECD through signing the multilateral CAA as master agreement in October 2014 several years have passed. The dynamic and challenging issue results in a number of new and/or extended requirements to design, operation and the management of modern technologies for taxes and regulations. Based on these growing regulatory challenges – with more or less unclear or more complex details – many financial institutions ensure the compliance through solutions which do not yet sufficiently represent the necessary degree of automation and the high performance requirements. Therefore, a number of financial institutions face the disillusioning situation that the RegTech solutions currently used demand optimisation regarding range and depth of market-driven requirements. SDS customers, however, have already started with the preparation of the next regulation wave with i:Reg for CRS/FATCA and are excellently prepared to fulfil the variety of requirements of the next generation quickly and in a highly professional manner. The reporting engine i:Reg is specifically designed for this purpose and provides the highest degree of automation for the typical reporting processes. Automatic data enrichment and automatic resolving of exceptions, handling the most complex issues and using the solution in several jurisdictions make i:Reg the best choice for large multinational groups and service providers – and preferred choice for leading, globally acting financial institutions.

Wrap-up of 4th Annual Post Trade Forum: Capital Markets, Regulations and New Technologies.

Almost exactly 10 years after the bankruptcy of Lehmann Brothers triggered the financial crisis, the Annual Post Trade Forum – which was already held for the 4th time – took place in Berlin. On 13-14th Sept, 2018, around 80 professionals from the securities services industry and financial market authorities across Europe and beyond met in the inspiring atmosphere of the Crowne Plaza to discuss a rich list of current hot topics. The presentations offered room to exchange opinions and the schedule provided enough time for a well-organised, relaxed walking tour through Berlin in the evening. We joined the event as sponsor and participants.

And it goes on … capital markets regulation, impacts and barriers

As opening session, Genni Caratozzolo from the European Commission gave a comprehensive update on the recent developments of the EU regulatory space.

A crucial point for the EU commission is the question whether a regulation really meets its purpose. Therefore, analysis work like EMIR REFIT is undertaken and more will follow. The expectation is that the progress on ongoing initiatives will help removing obstacles identified by the EPTF (European Post Trade Forum). Lots of progress has been made over the last years, yet there is still a busy EU regulatory agenda to cope with remaining obstacles and to address new challenges for the future.

This was a good starting point for more discussion about that progress and the expectations by the market, tackled by Werner Frey from AFME, who compared the results of the EPTF Report 2017 with the current regulation status. As known since then, the EPTF Report found out that 3 of the Giovannini post-trade barriers were removed, 8 partially removed and 4 not removed. In addition, the report identified a couple of new barriers and bottlenecks. A point of criticism was that the remaining barriers are legal and tax topics, which the public and not the financial sector is accountable for.

The estimated costs of WHT tax reclaim of EUR 8.4 bn per year in Europe and the lack of a common definition of “shareholder“ were stressed as one of the current issues. A slightly unsettling soundbite was “The next financial crisis will be caused by post-trade”.

SFTR Reporting

SFTR, together with CSDR, was the most present topic at this forum. The main information in the beginning: it´s not clear yet when live going will take place. The EU commission is still working on a regulation update which is expected for October 2018. Assumed that this is the reference date, the live going will then be expected for Q1 2020 for banks and investment firms.

Expected impacts of SFTR are the increase in transparency of SFTs and therefore the mitigation of systematic risk, as well as the way repos are processed today. This means a much higher level of automation, electronic trading and more standardised processes.

Although there is a good number of overlaps with EMIR reporting, many challenges for the SFTR implementation are waiting:

- Granular data requirements

- Strict LEI and UTI requirements

- Complexity of the transactions stemming from their individual specifics

- Information sources fragmentation

- Double-sided reporting obligation

- Global reach and multi-institutional effect

- The inter- and intra-trade repository (TR) reconciliation

Interesting and ready for download in this context: ICMA published the “Guide to Best Practice in the European Repo Market“.

CSDR and its impact

CSDR was the key topic of two presentations and one panel discussion. It is expected that CSDR will lead to more competition and consolidation and T2S is seen as the main driver. But competition and consolidation can be hindered by the remaining lack of EU cross-border harmonisation, including regulatory differences, variations in tax administration as well as corporate actions local requirements. As reminder, CSDR is not only relevant for CSDs, but all clients of every European CSD will be affected by dematerialisation, harmonisation of settlement periods, settlement discipline and reporting of internal settlements.

In general, CSDR is seen as a good thing which will need some time to develop and some questions will probably be answered later: will CSD monopolies stay “monopolies“ and will some of the well-functioning market specifics be kept? Moreover, the question came up how cryptocurrencies will be treated in the future. Is the cryptocurrency cash, a security, a fund or a commodity? Can the cryptocurrency be treated as CeBM (central bank money) or CoBM (commercial bank money)? We will see. In 5-10 years, much greater efficiency through technology and T+1 is expected.

What else…T2S and MiFID II transaction reporting

Beyond SFTR and CSDR, the lessons learned during the implementation of MiFID II transaction reporting were shown by Nordea Investment, which chose the way via ARM (Approved Reporting Mechanism).

Their biggest challenge was the quality of static data (as there is no guarantee whether the data is correct), which comes from multiple sources. Now, MiFID II transaction reporting helps Nordea to increase the quality of their data, which currently ends up with almost 100% acknowledgement of transaction reports by the NCA.

What are the implications of transaction reporting for Nordea? First, Nordea will force the business that all trades go over OTF`s, which will improve efficiency. Second, they recognise the need to “document everything”, and third, they will use transaction reporting as an internal tool to detect and avoid market abuse.

Another topic was the future of T2S. In short, one of the key statements was that post-trade costs may remain high for the next years because of the following reasons:

- T2S increased DVP price to 23.5 eurocents.

- Infrastructures have changed fee schedules ahead of T2S.

- Volume growth expectations may not be met due to increased CCP netting and expected future European economic growth rates.

- Further cost-drivers are ongoing harmonisation activities, new regulatory requirements (CSDR etc.) and practical experiences of T2S markets.

- Moreover, it was stated that the full benefits of T2S can only be seen after the removal of the EPTF barriers.

Technology innovations drive new business models

Of course, today no post-trade event can exist without some new technology sessions. This time, key topics were machine learning, digitalisation as well as client services and challenges by FinTechs. Obviously, a big advantage for the presenters of such topics is the chance to show more fancy, colourful and exciting slides than their regulatory predecessors (this is no criticism; this I would simply call a natural advantage).

Since one speaker cancelled, Chairman Philippe de Brossard jumped in with a good presentation about digitalisation in banks. He is of the opinion that for the digitalisation a bank should work on both digital processes and digital platforms. A data-driven approach is crucial to offer new valuable services to the customers, but still data is distributed in multiple banking systems today. The understanding of customer needs has to be the focus in all those transformations. Moreover, it is also important that the change of internal processes happens before providing new services to the clients, which in turns needs a new entrepreneurial, collaborative and innovative company culture.

Another session was about the challenges that FinTechs present the larger organisations. The main message: there is only one solution – a bank must invest with the vision to have an open, fully automated, flexible and scalable back-office operation with full transparency control of processes and process execution. To stay relevant against FinTechs, banks have 3 main operational levers: system, partnerships and leadership. The suggestion is to invest in the core systems, into your people and don´t be scared of partnerships.

Interesting side note: „The new front office is the back office which provides products“.

Concerning machine learning, two risks/obstacles were mentioned: the use of internal data due to GDPR and the increased risk of a cyber-attack.

How does SDS deal with these issues?

Our GEOS securities processing platform always complies with current regulatory requirements. We already dealt with the issue of MiFID II transaction reporting for our customers and are currently working on a good solution for SFTR and CSDR reporting. The successful implementation of T2S lies behind us and our customers are using SDS solutions highly satisfied in daily practice.

And we are steadily improving our existing product suite, exploring new products as well as working on the next technology and partnership models to embrace the upcoming chances for us and our customers.

Opportunities and possibilities of a universal tax engine for the financial industry.

The tax issue will in the near future remain an essential factor in the efforts of the financial industry towards achieving better regulatory compliance. Fragmented system environments, legacy systems which are difficult to maintain and a business segment-oriented silo architecture often pose an obstacle for an overall view of the customer as well as a reliable, correct tax treatment of his assets and transactions. Can the calculation, with-holding and certification of taxes by the financial service sector represent a future-oriented scenario for a central software solution?

The financial service sector has increasingly been involved in guaranteeing the tax conformity of its customers in Europe and worldwide during the last few years. This includes the calculation, retention, payment and reporting of taxes. In this light, the tax issue will remain a key factor in the financial industry’s efforts to improve regulatory compliance in the foreseeable future.

High complexity and diverse requirements

This is a challenging situation for the affected financial service sector in a number of ways. Frequent changes of the relevant legislation, confidential customer data, in particular duty to due care and attention, cost aspects and audit requirements represent a range of demands for IT, operations and management, which are difficult to balance. For internationally active groups, the complexity additionally increases due to the often significant differences in the country-specific tax laws.

Competence centres instead of silos

Fragmented system environments, legacy systems which are difficult to maintain and a business segment-oriented silo architecture often pose an obstacle for an overall view of the customer as well as a reliable, correct tax treatment of his assets and transactions.

Established application environments reach their limits with a classic silo architecture. They should be supplemented by applications which can handle taxes centrally and beyond multiple asset classes. This does not only facilitate the check of tax conformity, but also provides the technical basis for the creation of cross-country “competence centres”. It is important that such central applications represent cross-country as well as country-specific taxes in an appropriate, accordingly encapsulated form. Due to the mostly short implementation times for tax changes, the applications should also be able to represent a lot of functional logic through configuration instead of program logic.

A universal tax engine for the financial industry

Can the calculation, withholding and certification of taxes by the financial service sector represent a future-oriented scenario for a central software solution?

A centralised solution, which is based on the experiences of past years and considers the special challenges in this environment, maps the following design specifications:

- Taxes are country-specific

- Data demand and calculation logic can-not be determined with certainty at the time of solution design

- Cost and risks for operation and implementation are to be minimised

- Results must be explainable and transparent

- Handling of large transaction volumes must be possible

- Service-oriented architecture is to be supported

As a result: A general framework for tax calculation and the supply of tax-relevant data with high flexibility and reliability.

Conclusion

Especially in an environment of internationally largely uniform tax regimes such as, for example, double taxation agreements (DTAs), in particular US withholding tax, such a central special product for the international financial industry would make it possible to implement attractive and service-oriented solutions up to APIs for a future “banking as a platform” world.

For large institutions in particular, the cutting-edge architecture offers the chance to implement the sensitive issue of taxes in a more easily maintainable and manageable system environment.

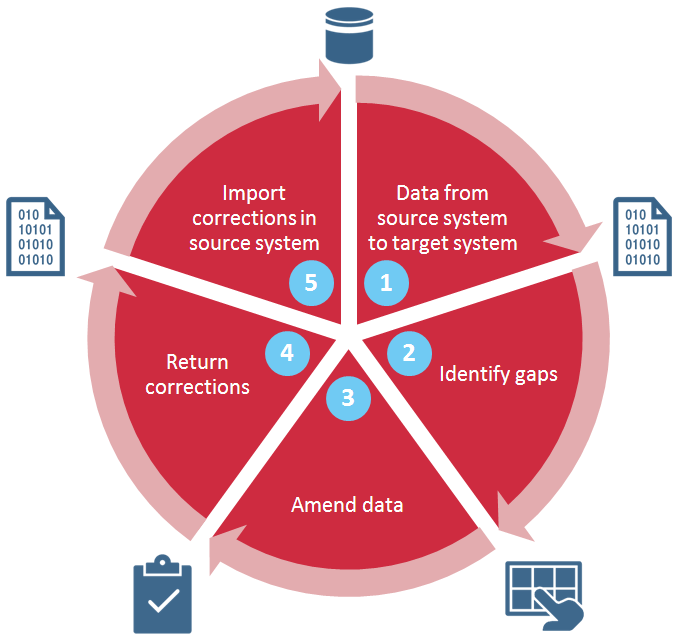

Data quality as a chronic challenge.

It is an unpleasant truth which people often tend to overlook: The master data is often not as good as one would like it to be. Specifically for CRS and FATCA reporting, very high data quality is required to generate correct and complete reports to the tax authorities. In practice, the data gaps that often remain can be time-consuming and expensive to correct. With our software solution i:Reg, these gaps are detected in time and can be eliminated by the financial institutions.

We are talking about data quality or, more accurately, insufficient data quality and how it can be permanently improved. Specifically for CRS and FATCA reporting, very high data quality is required to generate correct and complete reports to the tax authorities.

Today, financial institutions have clear and comprehensive requirements about which customer information must be recorded. Some requirements are legal, others come from internal processes. Fewer provisions and forms existed in the past and that poses challenges today regarding the completeness of the master data. Data gaps that arose this way are usually not corrected until the next customer meeting, some time in the future. For example, in 2015 CRS contained no requirements TIN verification or a validation checks.

Data gaps must be eliminated in the core system

It may be irrelevant to the core system of a financial institution whether a particular attribute is recorded for a customer. But it may still become a stumbling block when some later processing requires this information. Since the different downstream systems require different information, the list of attributes that are mandatory in the core system becomes very long, even when they are not absolutely necessary in the core system itself. So everything begins in the core system – either there is no field for certain information where the customer data is originally entered, or it was not mandatory to fill in these fields in the past.

Issue: mandatory fields

In fact, mandatory fields are a double-edged sword because, on the one hand, the customer should be completely recorded, but, on the other hand, the customer creation has to be fast and should not be blocked by details that can also be recorded later – provided, of course, that these subsequent additions are actually made. And provided that there is an adequate field for this purpose.

Whatever the cause, in the end there are often gaps in the data that can be time-consuming and expensive to correct.

Our software solution i:Reg detects data gaps in time

Due to the legal reporting obligations to international tax authorities, data gaps are especially unpleasant if they can prevent correct reporting. In order to create these complex reports it is now necessary to use a software product such as i:Reg. Because i:Reg detects and displays the gaps automatically, financial institutions become able to correct them systematically.

The gaps can be filled directly in i:Reg (so that at least the reports are correct), or this valuable information could be sent back to the data source – thus permanently improving the data quality for the benefit of other systems.

Conclusion

It pays off to correct the data quality directly at the source in order to avoid recurring problems while saving costs at the same time. In the words of John Wooden, “If you don’t have time to do it right, when will you have time to do it over?”

The GEOS community is growing.

GEOS ready for Linux / Oracle

An especially exciting topic for the entire community is the potential migration of GEOS instances to a Linux/Oracle environment. GEOS has already been in productive operation under Linux for several years, the optimised implementation for the database system Oracle has recently been carried out. There is already a first licensee for this configuration: ING DIBa Austria. First large-scale tests in the Oracle laboratory show that also the volumes of large customers can be processed without any problems. Further measures for performance optimisation have already been implemented and merely have to be verified to make sure that GEOS will be able to process the largest transaction volumes on the market under Linux/Oracle as well.

Regulatory topics 2018

Besides several final tasks regarding MiFID II, there are two potentially larger issues regarding the reporting regulations for SFTR and CSDR. In this context, the GDPR, for which we provided important functions in time, is of special interest. Whether additional work is required, also depends on the still pending regulation of the data protection authority and on the required interpretation of the regulation.

With the Adult Protection Law, which enters into force on 1 July 2018, another important task is to be accomplished. The required adaptations to the securities account master data, with which the roles of the individuals involved can be covered perfectly, will be carried out in due time.

The GEOS community is growing

By concluding a contract with Commerzbank for the takeover of settlement services, HSBC in Germany has won a large deal at the end of last year. This has substantially changed the settlement environment in Germany. By going live in 2020, the by far largest settlement unit on the German market will be created which leads to strong interest of the entire market in the development and success of the implementation project. Mr. Medler-Ulff, managing director of HSBC Transaction Services, gave an exciting and personal presentation and provided interesting insights into the project and the organisational measures for the agile implementation required due to the tight schedule.

This large project is not only interesting for HSBC Germany, but also for the entire community of GEOS users. It is a strong signal that GEOS is still state-of-the-art, and the most sustainable and best platform available for processing large volumes in our market.

We are also pleased to welcomeING-DiBa Austria among the direct licensees of GEOS. They decided to continue pursuing their growth plans on an individual instance of GEOS.

News from our product portfolio

User experience: Web UX Klimt

SDS delivers a new user interface. Web UX Klimt will provide an intuitive and modern web-based user interface for our products, based on the well-known framework Angular. The securities compliance tool c:Conform will be available as the first product in the new interface. Further existing and newly developed products will follow.

Automation in Exception Handling with artificial intelligence

Exception Handling is largely still manual work and presents a considerable part of the manual interventions in our applications. The potential of traditional methods of the automation has largely been exploited. In an exciting project we would like to further reduce the number of exceptions which must be manually edited. The methods considered for this purpose range from rule-based systems to the application of artificial intelligence.

Functional development

Besides technological innovations and the functional enhancements due to regulatory reasons we also offer new additional products to GEOS with the upcoming releases, e.g. for proxy voting, processing corporate actions according to target date “actual”, and in the area of parameterisation maintenance.

Conclusion

We are very happy about this successful event and the friendly atmosphere. We are looking forward to another event in autumn and would be delighted to welcome our customers again.